Posted inFinancial Literacy Mutual Fund

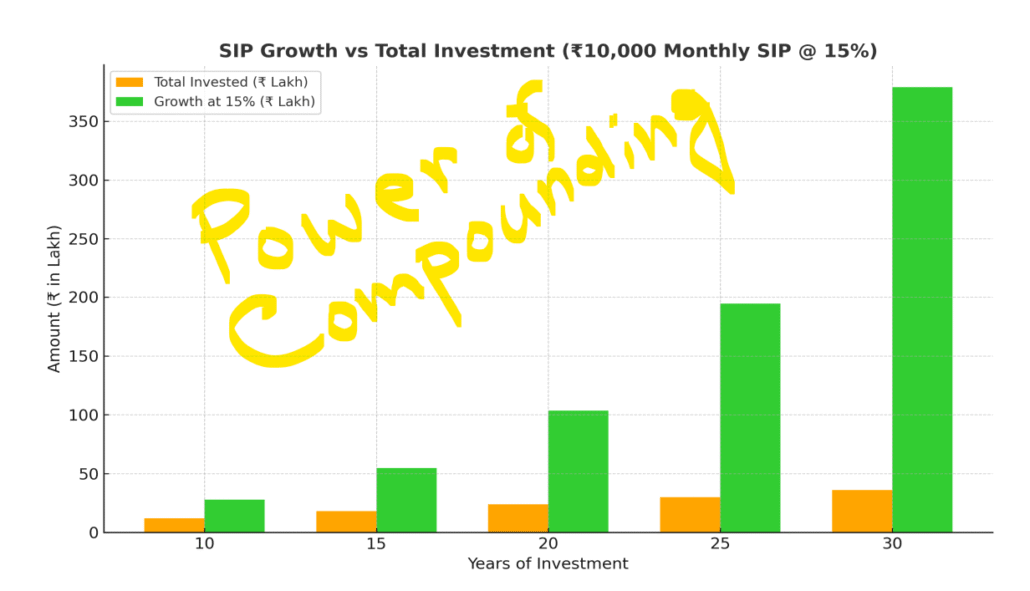

Beating Inflation India: How a 15% CAGR Small-Cap Mutual Fund Can Help

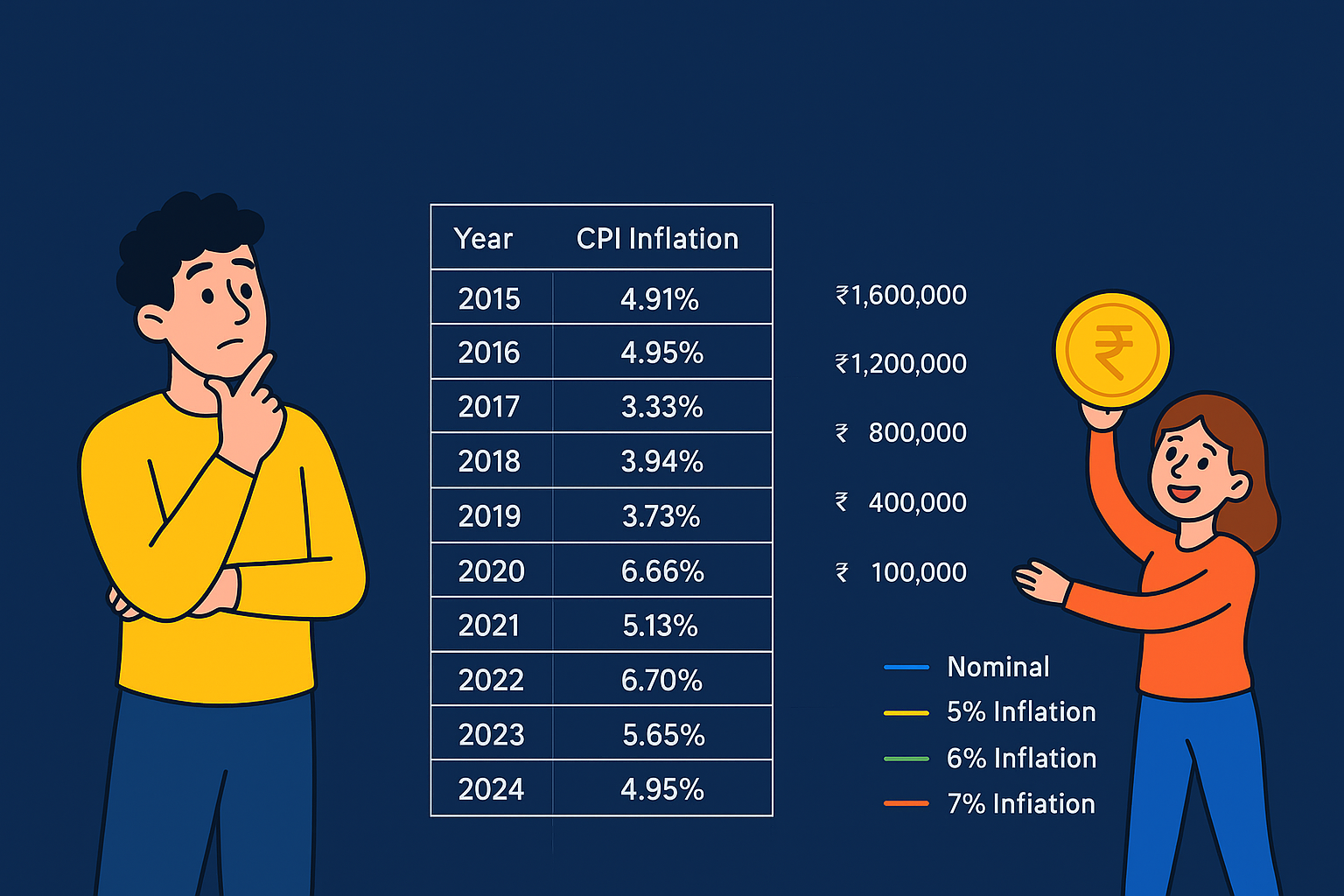

Key Takeaways: India’s inflation has averaged around 5–6% over the past decade, steadily eroding purchasing power. However, long-term investments in Mutual Fund small-cap schemes delivering around 15% CAGR can easily…