Why do most people panic at 65?

We dream of freedom at 65—yet bills, medicines, and family commitments don’t retire.

Without a plan, “later” becomes “too late.” A retirement plan SIP is how you take control.

🔑 Key Takeaways

At age 65, Indians usually fall into 4 categories – Broke, Still Working, Well-to-Do, or Wealthy.

Most (50–60%) end up financially vulnerable because of low pension coverage and poor planning.Data reality check:

~78% of elderly have no pension cover.

~40% fall in the poorest wealth segment.

~30–35% seniors still work to survive.

Your retirement category is not destiny – it depends on your financial planning, especially whether you start a retirement plan SIP.

Compounding favors early starters:

A 25-year-old inve

Corpus thumb rule: Target 25–30× annual retirement expenses to stay financially independent.

SIP = private pension: Unlike tiny government pensions, SIPs in equity mutual funds create a dependable, growing retirement income.

Blueprint for success:

Define your retirement lifestyle and target corpus.

Start SIPs in 2–3 equity + 1–2 debt funds.

Automate contributions.

Step up SIPs 10% yearly.

Rebalance and de-risk 5–7 years before 65.

Late starter? Don’t panic. You’ll need higher SIP amounts, but even beginning at 45 or 55 can still build meaningful wealth.

Do nothing = risk dependency. Without a retirement SIP, odds of being broke or still working at 65 are high.

👉 The ultimate message: Start a retirement plan SIP today. Small, consistent steps now can guarantee financial freedom and peace of mind at 65.

sting ₹5,000/month can retire with ₹5.9+ crore.

A 45-year-old investing ₹10,000/month builds only ₹1 crore.

Time matters more than amount.

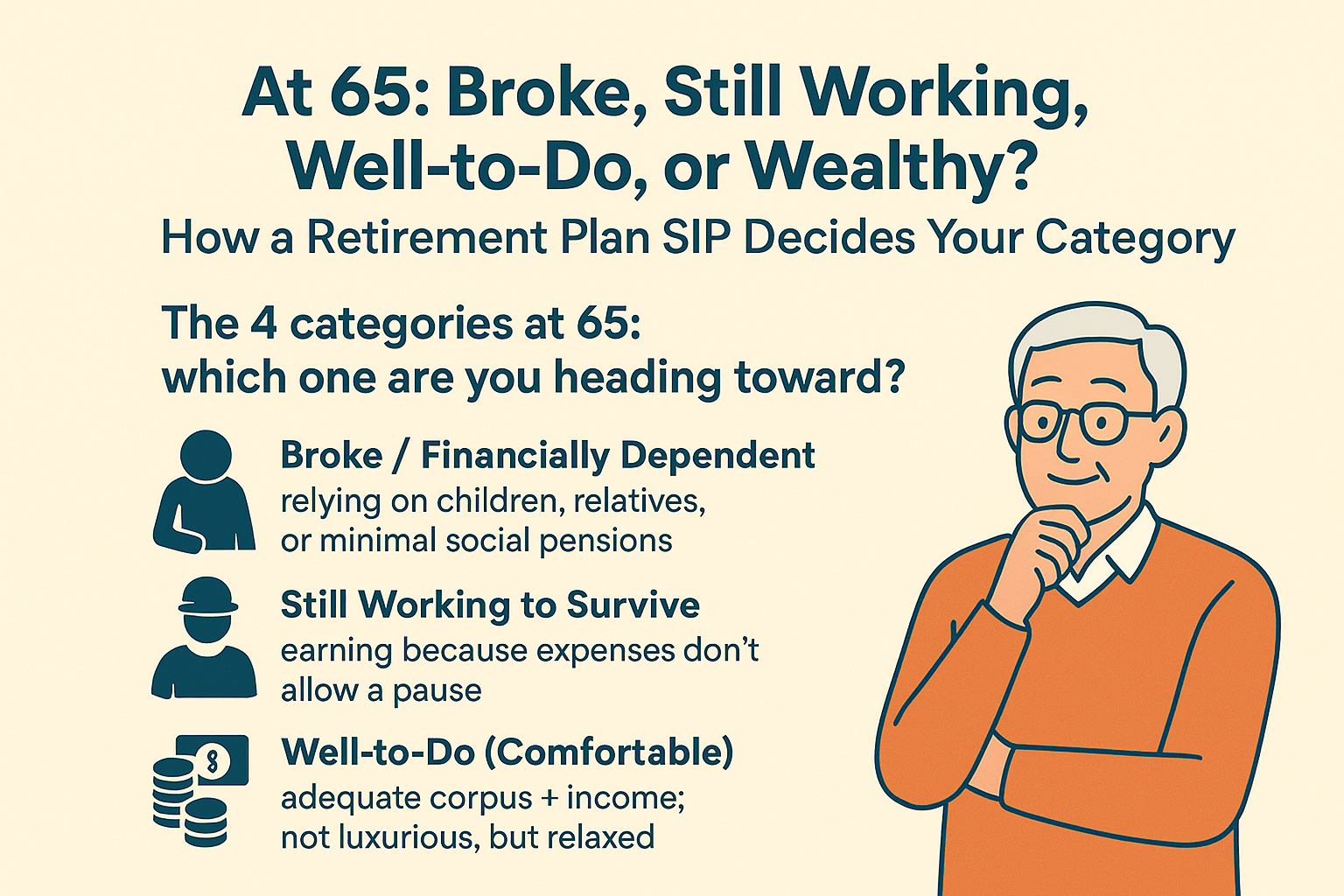

The 4 categories at 65: which one are you heading toward?

Let’s keep it brutally simple and deeply human:

-

Broke / Financially Dependent — relying on children, relatives, or minimal social pensions.

-

Still Working to Survive — earning because expenses don’t allow a pause.

-

Well-to-Do (Comfortable) — adequate corpus + income; not luxurious, but relaxed.

-

Wealthy (Financially Free) — corpus creates income that funds lifestyle + legacy.

There isn’t an official Indian government pie chart with these four exact labels. But we can triangulate credible indicators to build an indicative India snapshot:

-

Pension cover is low: A NITI Aayog senior-care report notes ~78% of India’s elderly live without any pension cover—a strong proxy for financial vulnerability. Source of information is from NITI Aayog

-

Poverty risk is real: UNFPA’s India Ageing Report (covered by mainstream press) highlights 40%+ of elderly in the poorest wealth quintile and ~18.7% with no income, underscoring dependence.

-

Many still work past 60: Research summarizing Indian data indicates elderly male workforce participation near ~49% and female near ~20%—netting roughly one-third of seniors still working.

Indicative 4-way segmentation for India (explained, not official):

-

Financially Vulnerable/Dependent (“Broke”): 50–60% (low pension coverage + high poverty share).

-

Still Working to Make Ends Meet: 30–35% (weighted by male/female senior LFPR).

-

Well-to-Do (Comfortable): 8–15%

-

Wealthy (Financially Free): 2–5%

These bands are reasoned estimates from India-specific signals above, not a government-issued pie. They’re a wake-up call—not a verdict. Your retirement plan SIP can move you from the left half of that pie to the right.

Quick Q&A: “Is this fear-mongering or facts?”

Q: “Are you saying most seniors are broke?”

A: The data says many are financially vulnerable because pension coverage is thin. A national policy report cites ~78% without pension. That doesn’t automatically mean “broke,” but it does mean high dependence unless you build your own income stream.

Why a retirement plan SIP beats “I’ll manage later”

A retirement plan SIP converts today’s small, automated investments into tomorrow’s dependable income. It’s habit + compounding + market growth—no drama, just discipline.

What return should we assume for long-term equity SIPs?

Historically, Indian large-cap equity (Nifty 50 Total Return Index) has delivered ~14% CAGR since 1999 (to 2021). To stay conservative and be future-safe, we’ll assume 12% CAGR in our examples.

Pick your age—see your “category-shifting” SIP number

Below are realistic, rounded projections for a retirement plan SIP at 12% CAGR till age 65. (They’re estimates, not guarantees. Markets fluctuate.)

| Start Age | Monthly SIP | Years | Estimated Corpus @65 |

|---|---|---|---|

| 25 | ₹5,000 | 40 | ~₹5.94 crore |

| 25 | ₹10,000 | 40 | ~₹11.88 crore |

| 35 | ₹5,000 | 30 | ~₹1.76 crore |

| 35 | ₹10,000 | 30 | ~₹3.53 crore |

| 45 | ₹10,000 | 20 | ~₹1.00 crore |

| 45 | ₹25,000 | 20 | ~₹2.50 crore |

| 55 | ₹10,000 | 10 | ~₹23 lakh |

| 55 | ₹25,000 | 10 | ~₹58 lakh |

Reality check: Time > Amount. A 25-year-old at ₹5k/month ends above ₹5 crore. A 55-year-old at ₹25k/month still struggles to reach ₹1 crore. Starting early is the real “alpha.”

“What corpus do I need to feel relaxed?”

A thumb rule: target 25–30× your annual retirement expense.

If you expect ₹12 lakh/year post-retirement, aim for ₹3–3.6 crore corpus.

Your retirement plan SIP bridges the gap—no windfalls needed.

The “Income from corpus” power: how comfort happens

If your corpus is ₹3 crore and you withdraw 3.5–4% annually, that’s ₹10.5–12 lakh/year before tax—enough for a well-to-do (comfortable) life for many families, plus growth to fight inflation. Your retirement plan SIP is basically building your private pension.

“But I have EPF/PPF. Why SIP?”

Great! Keep them. But note:

-

Social/old-age pensions are tiny (₹200–₹500/month centrally; states add varying top-ups—still modest). You must self-fund the lifestyle part.

-

Equity mutual funds (via SIP) historically capture India’s growth better than fixed-rate instruments over decades. That’s how you move from still working → well-to-do/wealthy.

The 6-step blueprint to start your retirement plan SIP today

-

Define “65 Lifestyle”

Note monthly expenses, medical buffer, travel, and gifts. Convert to annual need × 30 to get a corpus range. -

Pick asset mix

A starting glide path many planners use: Age in bonds (approx.) and rest equity. Example at 35: 35% debt / 65% equity via retirement plan SIP. Gradually raise debt as you near 65. -

Choose funds

-

Core: 1–2 Nifty 50/Nifty Next 50 Index Funds + 1 flexi-cap.

-

Optional satellites: 1 midcap for growth kicker; 1 short-duration debt fund for stability. (Total 4–5 funds max.)

-

-

Automate

Bank auto-debit on salary+2 days. Treat your retirement plan SIP like an EMI to your future self. -

Increase annually

Do a 10% step-up every year. Salary grows; so should your retirement plan SIP. -

Rebalance & de-risk

Once a year, rebalance to target allocation. Last 5–7 years before retirement, steadily move more to high-quality debt to protect the corpus you’ve built.

What if you started late?

Two levers: bigger SIP and longer runway (work a bit beyond 60 if health permits). Even a 45-year-old can reach ₹1–2.5 crore with ₹10–25k/month SIPs at 12% CAGR. Your retirement plan SIP is a powerful late-starter fix.

“If I do nothing—what then?”

Based on today’s signals, doing nothing increases the odds of being financially dependent or forced to work in your late 60s. Low pension coverage and meaningful senior workforce participation are strong warnings. Your retirement plan SIP is the simplest way to rewrite that outcome. NITI AayogIARIW

Action checklist (print this)

-

Decide your target corpus (25–30× annual spend).

-

Start a retirement plan SIP today (even ₹3–5k).

-

Pick 2–3 equity index/flexi funds + 1–2 debt funds.

-

Auto-debit + 10% step-up yearly.

-

Rebalance annually; de-risk 5–7 years before retirement.

-

Track once a year—then relax.

FAQs (for quick SEO + clarity)

1) How much SIP is enough for retirement?

Back-solve from corpus: Expense × 25–30. Use 12% assumed return to estimate the retirement plan SIP needed. Increase 10% yearly.

2) Are returns guaranteed?

No. Equity returns vary. We used 12% CAGR as a conservative long-term assumption vs Nifty 50 TRI’s ~14% since 1999.

3) Which is better—pension plans or mutual fund SIPs?

They solve different problems. Government social pensions are small; insurance pensions trade flexibility for guarantees. Retirement plan SIPs in equity funds historically build larger long-term corpuses. Blend as per comfort. Some of the information taken from The Economic Times

4) Should I stop SIPs when markets fall?

No. Falls are when SIPs buy more units. Retirement plan SIP = discipline through cycles.

5) How many funds are ideal?

4–5 total (2–3 equity + 1–2 debt) is plenty for 95% of investors.

6) Is a lump sum better than SIP?

If you have a large sum and long horizon, a phased STP into equity over 6–12 months is fine. For most, retirement plan SIP is simpler and emotionally easier.

7) What about healthcare and inflation?

Keep a separate health-insurance plan and allocate 10–15% of the corpus for medical buffer. Growth assets help counter inflation in a multi-decade retirement.

Key facts:-

-

Pension cover for elderly is low: NITI Aayog, Senior Care Reforms in India (2024): ~78% without pension cover.

-

Elderly poverty risk: UNFPA India Ageing Report 2023 (via coverage): 40%+ of elderly in poorest quintile; ~18.7% with no income.

-

Many still working post-60: Research summary shows elderly male WPR near 49%, female ~20%.

-

Equity long-term context: Nifty 50 TRI ~14.2% CAGR since 1999 (to 2021).

Final nudge (emotional close)

You don’t need luck to change your category at 65.

You need a retirement plan SIP that runs—quietly, automatically—while you live your life.

Start today, step it up yearly, and let compounding do the heavy lifting. Future-you will say, “Thank you.”

![]()

Pingback: Retirement Math Mistakes: How Small Errors Today Can Derail Your Future Plans - Cash Babu

Pingback: How to Withdraw Retirement Corpus Wisely After 55 - Cash Babu