Housewives Without Regular Income Get a Credit Card

Managing household finances is one of the most important tasks in every family. For housewives or homemakers, this can often be a challenging role, especially in today’s fast-paced economy where digital payments, online shopping, and contactless transactions have become the norm. But what if a housewife does not have a regular source of income? Many women wonder: Can a housewife apply for and use a credit card despite not earning a monthly salary?

The good news is – Yes, they absolutely can! Although the application process and eligibility criteria differ from salaried or self-employed applicants, there are multiple financial products designed specifically for homemakers. In this comprehensive guide, we will cover:

- The importance of credit cards for housewives

- How to apply for a credit card without regular income

- Eligibility criteria and required documents

- Best credit card options for housewives in India

- Benefits of owning a credit card

- Common challenges and how to overcome them

- Responsible usage tips

- Frequently Asked Questions (FAQs)

- Real-life success stories

- Conclusion

Why Credit Cards Matter for Housewives

Financial Independence

For decades, homemakers often depended on cash or required permission from family members to make purchases. Owning a credit card empowers housewives with financial independence, allowing them to manage daily expenses such as groceries, utility bills, and medicines without relying on others.

Emergency Support

Life is unpredictable. Emergencies—medical, household repairs, urgent travel—can strike without warning. A credit card provides instant access to funds, helping a housewife handle emergencies promptly without stressful delays.

Building Credit History

In India, having a good credit score is important for future financial activities, such as applying for personal loans, home loans, or car loans. Even without a regular income, having a credit card and maintaining timely payments builds a positive credit history, helping homemakers establish their financial identity.

Exclusive Rewards and Offers

Many credit cards offer cashback, reward points, discounts, and exclusive deals on groceries, utility bill payments, shopping, and dining. Homemakers can turn everyday expenses into savings or rewards, giving added financial benefit.

How Can Housewives Get a Credit Card?

Let’s explore the most common and accessible ways a housewife can obtain a credit card in India.

1. Add-on / Supplementary Credit Card

An add-on card is linked to the primary credit card account held by the spouse or a family member. The credit limit is shared between the primary and add-on cardholder. Key points:

- Minimal paperwork required.

- Easy to apply through the bank’s online or offline process.

- Shared credit limit means spending affects the primary cardholder.

- Full access to reward points, offers, and EMI facilities.

2. Secured Credit Card

A secured credit card is backed by a fixed deposit (FD) in the bank. The bank offers a credit limit based on the FD amount, typically 75–85% of the deposit.

- Best for housewives without income proof.

- Requires documents like ID proof, address proof, and FD receipt.

- Safer for the bank and ideal for building credit history.

- Low annual fees and straightforward approval process.

3. Joint Credit Card Application

A joint application with a spouse or another earning family member allows the housewife to become a co-holder.

- Both applicants share responsibilities.

- Credit limit and benefits apply equally.

- Builds individual credit history.

4. Credit Card Against Savings or Investments

Certain banks offer credit cards against the applicant’s savings account balance, mutual funds, or insurance policies.

- The bank evaluates the total value of the financial asset.

- Helps secure a card without income proof.

- Ideal for conservative use and emergencies.

Eligibility Criteria for Housewives

Even though the process is relatively straightforward, banks have specific criteria:

- Age: Typically between 21 and 65 years.

- Identity Proof: Aadhaar Card, PAN Card, Passport, Voter ID.

- Address Proof: Utility bill, Aadhaar Card, Driving License.

- Relationship proof: In case of add-on card, a marriage certificate may be required.

- Fixed Deposit (for secured cards): FD account in the same bank.

- Savings Account: Banks may require the housewife to have a savings account with them.

Documents Required

Here is a complete list of documents a housewife may need while applying:

| Document Type | Examples |

|---|---|

| Identity Proof | Aadhaar Card, PAN Card, Passport |

| Address Proof | Utility Bill, Aadhaar, Driving License |

| Relationship Proof | Marriage Certificate |

| Fixed Deposit Receipt | For secured card applications |

| Savings Account Details | Bank passbook or statement |

Best Credit Card Options for Housewives in India

➤ Add-on Cards

These are easy to get and managed under the primary account holder:

- SBI Add-on Credit Card

- HDFC Add-on Credit Card

- ICICI Add-on Credit Card

- Axis Bank Add-on Credit Card

➤ Secured Credit Cards

Great for those who want an independent card without income proof:

- SBI Advantage Plus Secured Credit Card

- Axis Bank Insta Easy Credit Card

- ICICI Instant Platinum Secured Credit Card

➤ Lifestyle Credit Cards

Some banks offer cards targeted toward frequent shoppers and grocery buyers, even to homemakers, especially if backed by FD or as an add-on.

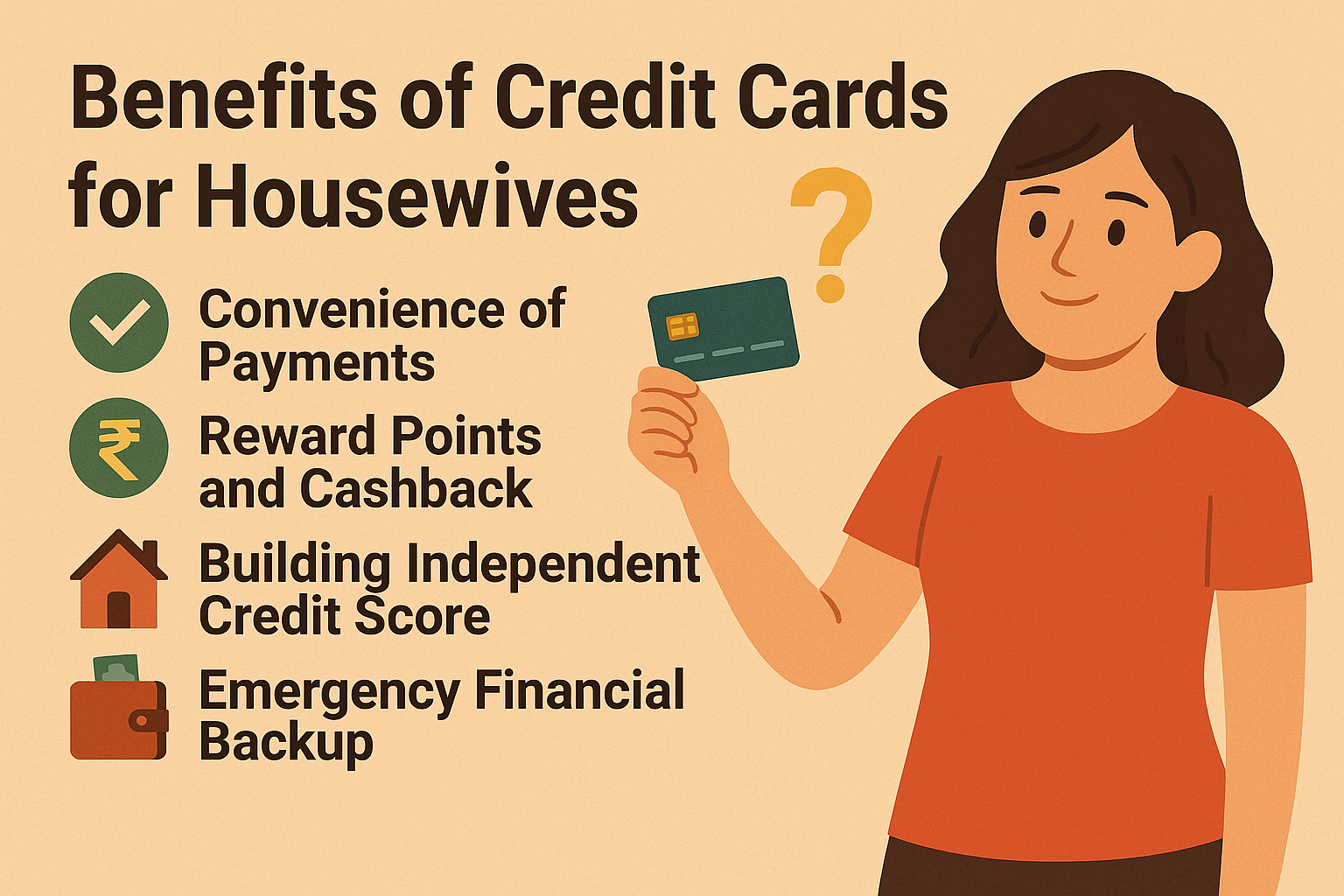

Benefits of Credit Cards for Housewives

✅ Convenience of Payments

Cashless payments for groceries, utility bills, medicines, and online purchases.

✅ Reward Points and Cashback

Earn rewards on everyday transactions, helping reduce monthly expenses.

✅ Building Independent Credit Score

Good credit behavior builds an individual credit score, helpful for loans in the future.

✅ Emergency Financial Backup

Provides peace of mind for sudden emergencies.

Common Challenges Housewives Face and How to Overcome Them

⚠️ Challenge: No Income Proof

Solution: Opt for a secured credit card or add-on card.

⚠️ Challenge: Fear of Overspending

Solution: Start with a low credit limit and set monthly usage goals.

⚠️ Challenge: Managing Timely Payments

Solution: Set up auto-pay or reminders to avoid interest and penalties.

Responsible Credit Card Usage Tips

- ✅ Always pay bills before the due date.

- ✅ Monitor monthly expenses using bank apps or spreadsheets.

- ✅ Avoid using the full credit limit. Keep utilization below 30%.

- ✅ Use the card for planned purchases, not impulsive spending.

- ✅ Opt for reward categories you frequently use (e.g., groceries).

Frequently Asked Questions (FAQs)

Q1: Can a housewife apply for a credit card without income proof?

A: Yes, through add-on cards, secured credit cards, or joint applications.

Q2: Is a credit card safe for housewives?

A: Yes, as long as it is used responsibly, and payments are made on time.

Q3: Will a secured credit card affect my savings?

A: The fixed deposit serves as collateral and continues to earn interest.

Q4: Can I convert my credit card debt into EMI?

A: Yes, most credit card issuers offer EMI conversion for large purchases.

Q5: What is the difference between an add-on card and a supplementary card?

A: There is no difference. Both terms refer to a card issued under the primary cardholder’s account, allowing another family member (like a housewife) to use the same credit limit and benefits.

Q6: How is my credit limit determined if I apply for a secured credit card?

A: Typically, the credit limit is 75–85% of the fixed deposit amount you place with the bank. For example, if you deposit ₹1,00,000, your credit limit may be ₹75,000 to ₹85,000.

Q7: Can a housewife apply for a credit card independently in India?

A: Yes, but it may require supporting financial documents such as fixed deposits, savings account balances, or being a co-applicant with a spouse.

Q8: Are there annual fees for secured or add-on credit cards?

A: Most secured and add-on credit cards have lower annual fees compared to regular credit cards. Some banks may even offer no-fee options for first-time users or homemakers.

Q9: How long does it take to get approval for a secured credit card?

A: Once the fixed deposit and documents are submitted, approval typically takes 7 to 15 business days.

Q10: Can using a credit card improve my CIBIL score?

A: Yes, regular and timely payments on a credit card positively impact your credit score, even if there is no regular income, as long as the bank reports your activity to credit bureaus.

Q11: Are reward points on credit cards useful for homemakers?

A: Absolutely. Many cards offer points for grocery shopping, utility bill payments, and daily essentials—categories that a housewife frequently uses. These points can later be redeemed for vouchers, discounts, or even cashback.

Q12: Can I use my credit card internationally if I’m a homemaker?

A: Yes, many credit cards are valid for international use, but it is important to notify the card issuer before traveling abroad and be aware of foreign transaction fees.

Q13: Is it mandatory to link a savings account for a secured credit card?

A: Typically, yes. A savings account helps the bank manage the fixed deposit collateral and facilitates transactions such as bill payments and auto-debit.

Q14: What happens if I miss a payment on my credit card?

A: Missing payments can attract high-interest charges and penalties. It may also negatively impact your credit score. Setting up auto-pay or reminders is highly recommended.

Real-Life Success Stories

📖 Case Study 1: Rekha’s Journey to Financial Independence

Rekha, a homemaker from Pune, was hesitant to apply for a credit card at first. She applied for a secured card backed by an FD of ₹50,000. With this card, she managed household expenses efficiently, started building a credit score, and even enjoyed cashback on groceries.

📖 Case Study 2: Priya’s Emergency Lifesaver

Priya, from Jaipur, had no regular income but became an add-on cardholder under her husband’s primary credit card. During a medical emergency, the card allowed her to arrange treatment without delays, avoiding stressful borrowing from relatives.

Conclusion

In today’s evolving financial landscape, housewives without a regular source of income are not left behind when it comes to accessing credit facilities. In fact, financial independence and empowerment have become increasingly important for homemakers, especially as digital transactions and cashless payments grow more prevalent. Contrary to the common myth that credit cards are only for salaried individuals, there are multiple practical and accessible options available for homemakers.

Housewives can apply for credit cards through several channels, including add-on or supplementary cards under a family member’s primary credit card, secured credit cards backed by a fixed deposit, joint credit card applications, or credit cards issued against investments or savings accounts. These options are specifically designed to accommodate those without regular income while maintaining financial security for banks.

Owning a credit card brings more than just convenience in making everyday purchases—it plays a crucial role in empowering homemakers by giving them:

-

✅ Financial Independence

Homemakers no longer need to rely on cash transactions or ask family members for small but important expenses such as grocery shopping, utility payments, medicines, or school-related fees for children. A credit card provides easy access to funds, enabling timely and secure payments. -

✅ A Safety Net for Emergencies

Emergencies, such as sudden medical expenses or urgent home repairs, require fast financial solutions. A credit card offers a ready cushion, allowing housewives to tackle these unexpected challenges without the stress of scrambling for immediate cash or loans. -

✅ A Path to Build Personal Credit History

Building a strong credit history is essential for future financial milestones, such as applying for home loans, personal loans, or car loans. Regular usage of a credit card and disciplined repayment behavior helps establish a good credit score, building a foundation of financial credibility in one’s own name. -

✅ Attractive Rewards and Cashback Offers

Modern credit cards come with attractive reward programs and cashback offers specifically suited for everyday expenses. From groceries and utility bill payments to shopping and dining, housewives can make their daily expenditures more rewarding and cost-effective.

However, simply owning a credit card is not enough. Responsible usage is key to reaping its full benefits. Housewives should start with a lower credit limit to manage spending effectively and gradually increase it over time as they build confidence. It is important to set a monthly budget, track expenses, and always ensure that the credit card bills are paid on time to avoid unnecessary interest and penalties.

Furthermore, understanding the terms and conditions of the card, being aware of the grace period, and knowing when reward points expire are essential habits for maximizing the card’s utility. Tools like auto-pay facilities, mobile banking apps, and alerts can simplify financial management, making the credit card a safe and efficient financial companion.

In essence, a credit card serves as a powerful financial instrument for homemakers—not just for shopping, but as a means of promoting financial independence, securing future creditworthiness, and providing peace of mind in emergencies. With careful planning, disciplined usage, and awareness of available options, housewives can significantly improve their financial well-being and contribute actively to the family’s financial growth.

By taking small steps today—such as applying for a secured credit card or becoming an add-on cardholder—housewives can embark on a journey toward financial empowerment. The key lies in making informed choices and using the card as a tool for responsible financial management, rather than as an opportunity for overspending.

Ultimately, the credit card becomes more than just plastic in the wallet—it becomes a symbol of empowerment, financial freedom, and a stepping stone toward a secure and independent financial future.

![]()